Deep Diving into DeFi: Decentralized Lending and Borrowing

1 year ago By Blockchain Mata

In recent years, DeFi has exploded in popularity, offering users an alternative to traditional banking and financial institutions. One of the most fascinating areas of DeFi is decentralized lending and borrowing, which allows users to lend and borrow cryptocurrencies without the need for intermediaries.

In this blog, we will dive deep into the world of decentralized lending and borrowing, exploring its benefits, risks, and the platforms that make it possible. Get ready to learn all about this revolutionary aspect of DeFi!

Decentralized Lending and Borrowing:The Challenges Tackled.

The financial industry's lending and borrowing services, enabled by credit and collateralization, have seen a significant increase, with borrowing volume rising to $9.7 billion in April 2021 - a 102-fold increase from the previous year.

This system has historically played a crucial role in spurring economic activity and enabling individuals to obtain funds for various purposes, such as starting a business or buying a house.

However, it requires trust and an intermediary, often provided by banks, with a complex credit system used to assess borrowers' ability to repay loans and other requirements.

The current lending and borrowing system faces challenges like strict funding criteria, limited accessibility to banks due to geographical or legal restrictions, high barriers to loan approval, and exclusivity of low-risk high-returns lending for the wealthy.

In contrast, in the DeFi landscape, anyone with enough collateral can access capital without the need for banks. Decentralized liquidity pools allow anyone to lend and contribute to these pools, and borrowers can repay with algorithmically-determined interest rates.

Unlike traditional bank loans with stringent KYC and AML policies, collateral is the only requirement for obtaining a loan in DeFi.

In the next sections, we will explore how Compound Finance and Aave, the top DeFi lending and borrowing protocols, enable such bankless lending and borrowing mechanisms.

Compound Finance

Compound Finance is a decentralized finance (DeFi) protocol that allows users to earn interest on their cryptocurrency holdings and borrow cryptocurrencies. It operates on the Ethereum blockchain and uses a system of algorithmically determined interest rates.

Users can deposit their cryptocurrency into the protocol and earn interest in the form of cTokens, which can then be used as collateral to borrow other cryptocurrencies. The interest rates are determined based on supply and demand for each cryptocurrency within the protocol.

As a liquidity pool built on the Ethereum blockchain, Compound Finance enables lenders to earn interest on their idle funds and borrowers to borrow funds for productive or investment use, with interest rates determined by algorithms that take into account supply and demand of the assets.

Compound simplifies the lending and borrowing process by allowing suppliers and borrowers to interact directly with the protocol for interest rates, creating a more efficient money market.

What are cTokens?

cTokens, or Compound Tokens, are digital tokens that are minted when users supply assets to the Compound protocol. For example, if a user supplies 100 USDC to the protocol, they would receive 100 cUSDC tokens in return.

These cTokens represent the user's share of the total supply of that asset in the Compound liquidity pool, and they earn interest based on the interest rate of that asset on the Compound protocol.

cTokens are ERC-20 tokens that can be transferred and traded just like other tokens on the Ethereum blockchain. They can also be used as collateral for borrowing other assets on the

Compound platform. When a user wants to redeem their underlying assets from the Compound protocol, they can simply burn their cTokens to receive the equivalent amount of the underlying asset, plus any accrued interest.

By using cTokens, Compound makes it easy for users to earn interest on their idle assets and provides a more efficient way to lend and borrow assets on the Ethereum blockchain.

How to start earning interest on Compound

To start earning interest on Compound, you will need to follow these general steps:

Set up an Ethereum wallet: You will need an Ethereum wallet that supports the interaction with smart contracts, such as MetaMask.

Get some assets: You will need some digital assets that are supported by the Compound protocol, such as USDC, DAI, or ETH.

Connect your wallet to Compound: Use a web3 interface like Etherscan or MyEtherWallet to interact with the Compound smart contracts and connect your Ethereum wallet to the Compound protocol.

Supply your assets to the Compound protocol: Once you are connected to the Compound protocol, you can supply your assets to the liquidity pool and start earning interest. When you supply assets to the protocol, you will receive cTokens that represent your share of the total supply of that asset in the pool.

These cTokens will accrue interest based on the interest rate of that asset on the Compound protocol.

Monitor your earnings: You can monitor your earnings and redeem your underlying assets and interest at any time by burning your cTokens and withdrawing your assets from the protocol.

Note that using Compound involves risks, and it's important to understand the risks involved before participating. Make sure to do your own research and understand the potential risks and rewards before supplying assets to the Compound protocol.

Borrowing on Compound

To borrow on Compound, you need to supply collateral, and the more assets you supply, the more you can borrow.

Different assets have different collateral factors that determine how much you can borrow. Borrowed assets are sent directly to your Ethereum wallet.

A portion of the interest paid by borrowers goes to the Compound reserve, which is controlled by COMP token holders, and each supported asset has its reserve factor that determines how much goes into the reserve.

How much interest will you receive, or pay?

The amount of interest that someone receives or pays on Compound depends on several factors, including the specific asset being supplied or borrowed, the current market supply and demand for that asset, and the amount of funds supplied or borrowed.

The interest rates are denoted in Annual Percentage Yield (APY), and they can fluctuate over time.

Using the DAI stablecoin as an example, a lender would earn 4.45% APY

(as of January 2021) in a year, while a borrower would be paying 6.44% APY

interest after a year.

It is important to do your own research and understand the risks involved in lending or borrowing on the Compound platform before participating.

Do I need to register for an account to start using Compound?

To use the Compound protocol, you do not need to register for an account in the traditional sense. Compound is a decentralized protocol built on the Ethereum blockchain, so you can access it directly through an Ethereum wallet that supports the interaction with smart contracts.

To interact with Compound, you will need to have some funds in an Ethereum wallet, such as MetaMask, and use a web3 interface such as Etherscan or MyEtherWallet to interact with the Compound smart contracts. You can then supply funds to the liquidity pool and earn interest or borrow funds and pay interest.

It is important to note that using decentralized finance protocols like Compound involves risks, such as the possibility of smart contract bugs, market volatility, and other factors that may affect the value of your funds. Do your own research and understand the risks involved before participating.

Compound Governance

Compound Governance is a system that allows users who hold the native COMP token to propose and vote on changes to the Compound protocol. COMP token holders can create a proposal to change any parameter of the protocol, such as adding or removing assets, changing interest rates, or adjusting other system parameters.

To create a proposal, a user must hold a minimum amount of COMP tokens and submit it to the Compound Governance system.

Once the proposal is submitted, it is open for voting by other COMP token holders. If the proposal receives a certain threshold of votes and passes a minimum quorum, it can be implemented into the Compound protocol.

The governance system is designed to promote decentralization, community involvement, and transparency in the development and evolution of the Compound protocol. It allows users to have a direct say in the future of the protocol and enables them to propose and vote on changes that they believe will benefit the ecosystem as a whole.

Price Movement

If the value of the collateral used for a loan on Compound goes up, the collateral ratio also goes up, allowing for a bigger loan if desired.

However, if the collateral value goes down and the collateral ratio falls below the required minimum, the collateral will be partially sold off with an 8% liquidation fee to achieve the minimum collateral ratio, which is known as liquidation.

Liquidation

Compound Finance is a decentralized finance (DeFi) platform that allows users to earn interest on their cryptocurrency deposits and borrow other cryptocurrencies using their deposits as collateral.

In the context of Compound Finance, liquidation refers to the process of automatically selling a borrower's collateralized assets if their loan becomes undercollateralized due to a drop in the value of their collateral.

Liquidation happens when the value of collateral is lower than borrowed funds, and the current liquidation fee is 8%. It ensures excess liquidity and protects lenders against default risk.

What is Aave

Aave is a decentralized money market protocol that allows users to lend and borrow 24 different assets, offering more assets than Compound. Aave and Compound operate similarly, where lenders can provide liquidity and earn interest, while borrowers can take loans and pay interest.

However, Aave is more complex and offers more flexibility and features compared to Compound. Keep an eye out for future articles on this space, deep diving and comparing these two protocols.

For now, let's look at the eight key features of Aave.

1. Decentralization: Aave operates on a decentralized, peer-to-peer network, allowing users to transact directly with each other without intermediaries.

2. Non-Custodial: Aave is a non-custodial platform, meaning users retain full control of their funds at all times.

3. Multiple Asset Support: Aave supports a wide range of assets, including cryptocurrencies, stablecoins, and tokenized real-world assets.

4. Flash Loans: Aave offers flash loans, which are uncollateralized loans that can be taken out and repaid within the same transaction.

5. Liquidity Pools: Aave uses liquidity pools to ensure that funds are always available for borrowing, reducing the risk of loan defaults.

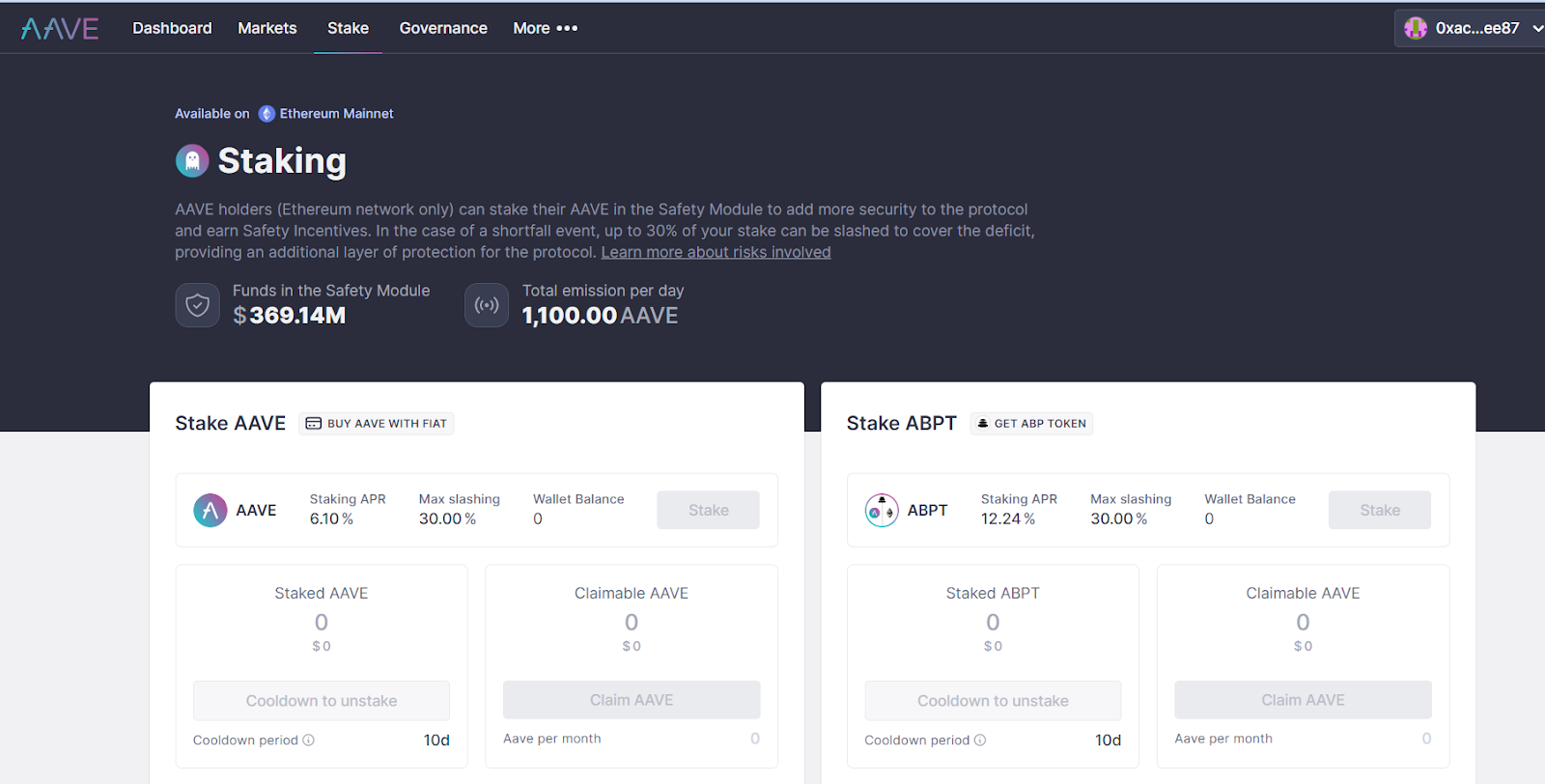

6. Staking: Aave provides an opportunity for users to earn rewards by staking Aave tokens and providing liquidity to the platform.

7. Tokenization: Aave allows users to tokenize their assets, making it possible to trade and lend assets that are traditionally difficult to access.

8. Low fees: Aave has low fees compared to traditional lending platforms, providing users with more access to funds at a lower cost.

Aave Governance and how it works

Aave is a decentralized finance (DeFi) protocol that allows users to lend, borrow, and earn interest on cryptocurrencies. Aave's governance system operates on the Ethereum blockchain and is based on a decentralized autonomous organization (DAO) structure.

Aave's governance is managed through its native token, AAVE, which allows token holders to participate in decision-making processes related to the protocol. Token holders can propose and vote on changes to the protocol, such as adding or removing assets, changing interest rates, and modifying governance parameters.

Proposals are submitted through the Aave governance forum and require a certain amount of support from AAVE token holders to be eligible for a vote. Once a proposal reaches the required support threshold, it is put to a community vote, and the decision is made based on a quorum of the total AAVE supply and a simple majority of votes.

In addition to the community governance process, Aave has a team of core developers who maintain and improve the protocol's technical infrastructure.

The Aave Improvement Proposal (AIP) process provides a structured framework for developers to propose technical changes to the protocol that require community review and approval.

To start earning interest on Aave

Similar to Compound Finance, when you supply assets to the Aave protocol, you receive a corresponding amount of aTokens, which represent your underlying assets and start earning interest immediately.

However, you won't receive the interest until you redeem your aTokens. The interest is paid out in the same cryptocurrency as the asset you supplied, and the amount you receive will depend on the current interest rate at the time of redemption.

Borrowing on Aave

Before you can start borrowing on Aave, you need to deposit an asset as collateral. The amount of collateral you need to deposit must be higher than the amount you want to borrow, and the maximum amount you can borrow is determined by the preset Loan to Value (LTV) ratio for the specific asset you're using as collateral. Each asset on Aave has a different LTV, ranging from 15% to 80%.

If the LTV for your collateral reaches the liquidation threshold, liquidators can sell up to 50% of your position to cover the outstanding debt, and you may also be subject to a liquidation penalty.

Note that not all assets can be used as collateral, as tokens with a single counterparty risk exposure cannot be used due to the risk of draining the protocol of all liquidity.

How much interest will you receive or pay?

The interest rates for both borrowers and lenders on Aave are determined algorithmically, based on the supply and demand for each asset.

When the borrowing demand is high and there is less available liquidity in the pool, the interest rates will increase, which means that lenders can earn more interest. As of April 2021, the APY for lenders who deposited USDT on Aave was 5.99%.

Borrowers on Aave can choose between variable or stable interest rates, with the variable interest rate for USDT at 3.97% APR and the stable interest rate for USDT at 11.99% APR. However, it's important to note that these rates are subject to change over time based on market conditions and the supply and demand for each asset on the platform.

Choosing interest rate

Stable- and Variable Annual Percentage Rate (APR)

Stable Annual Percentage Rate (APR) is a fixed rate that may change over time under certain market conditions, while Variable Annual Percentage Rate (APR) is a fluctuating rate determined by supply and demand in the Aave protocol.

Stable rate borrowers prefer knowing the exact amount of interest to be repaid and are less impacted by liquidity fluctuations, while variable rate borrowers are subject to interest rate changes based on available liquidity.

Do I need to register for an account to start using Aave?

Aave is a decentralized protocol that allows users to connect their wallets and start lending or borrowing without the need to create an account or go through a centralized registration process.